Market Scenario

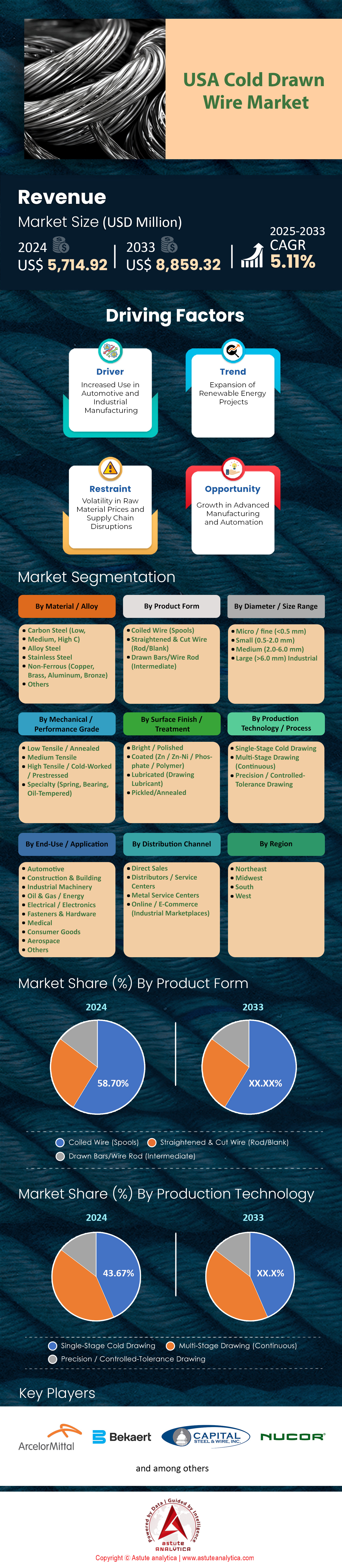

U.S. cold drawn wire market size was valued at US$ 5,714.92 million in 2024 and is projected to hit the market valuation of US$ 8,859.32 million by 2033 at a CAGR of 5.11% during the forecast period 2025–2033.

Key Findings

- Based on material/alloy, carbon steel (low, medium, high C) holds the largest share of 51.42% in the US cold drawn wire market.

- Based on product form, coiled wire (spools) holds the largest share at 58.70%, reflecting its widespread use in continuous-feed applications.

- Based on diameter/size range, medium size range (2.0–6.0 mm) dominates the market with 38.97% share.

- Based on mechanical/tensile grade, medium tensile holds the largest share of 34.33%.

- Based on application, automotive segment leads with 29.72% share, driven by its extensive use in fasteners, springs, and structural components.

- Based on distribution channel, direct sales account for the largest share at 46.38%.

The demand for cold drawn wire across the United States is currently experiencing a profound structural shift, moving beyond typical cyclical recovery into a period of sustained, high-volume requirement. Federal policy has successfully transitioned from legislative planning to active procurement, serving as the primary catalyst for the US cold drawn wire market. The Department of Transportation catalyzed this momentum in July 2024 by awarding US$ 5 billion specifically for large bridge projects. These grants are not merely budgetary allocations; they are actively funding the repair or replacement of 11,400 distinct bridge sites. 18 of these critical structures, each carrying over 1.2 million vehicles daily, received individual grants exceeding US$ 100 million. Consequently, manufacturers are ramping up production of prestressed concrete strand and heavy-gauge wire mesh to meet strict federal delivery timelines.

Simultaneously, a historic re-shoring of industrial capacity is creating a secondary engine of growth in the US cold drawn wire market. Total construction spending on US manufacturing plants reached an unprecedented US$ 234 billion for the full year 2024. The intensity of this build-out is evident in monthly investment rates, which hit US$ 21.1 billion in late 2024. Since 2019, spending in this sector has surged by an absolute 242%, driven largely by semiconductor and clean energy manufacturing incentives. 94% of the rise in non-residential construction spending during 2024 was attributable solely to data centers and factories. Such concentrated heavy construction establishes a new, elevated consumption baseline for the US cold drawn wire market, decoupling it from softer commercial retail trends.

To Get more Insights, Request A Free Sample

Consumption Baselines and Volume Metrics

Quantifying this surge reveals a market operating at high utilization. While total steel shipments provide a macro view, specific indicators paint a clear picture of wire consumption. Nucor Corporation, a bellwether for the industry, shipped 24.8 million tons of steel in 2024, maintaining a mill utilization rate of 74% in Q4. Industrial put-in-place spending is projected to close 2025 at US$ 232 billion, ensuring that the volume of wire mesh required for concrete slabs remains near record highs.

Residential construction provides an additional layer of stability for the US cold drawn wire market. Developers are forecast to initiate 1.35 million housing starts in 2025, following a solid 2024 performance of 1.367 million starts. Single-family homes, a key consumer of concrete reinforcement, stabilized at an annual rate of 890,000 units by August 2025. Furthermore, the automotive sector contributed significantly to the consumption of cold heading quality (CHQ) wire, with US light vehicle production totaling 15.85 million units in 2024. Even with a revised forecast of 14.9 million units for 2025, the sheer scale of fastener and spring production keeps wire drawing benches running continuously.

Geographic Hotspots: Top Five States Driving Consumption

Geography plays a pivotal role in demand distribution, with five key states anchoring the US cold drawn wire market.

- Texas: The state remains the undisputed leader in volume, driven by a convergence of energy infrastructure and population growth. With a robust pipeline of highway expansion and the hardening of the ERCOT grid, Texas commands a significant share of heavy-gauge wire shipments.

- California: Innovation and grid resilience define California's demand. The "CHARGE 2T" project alone will reconductor 100 miles of transmission lines, requiring specialized high-tensile wire. Additionally, the state leads the solar push, contributing heavily to the 11.7 GW of solar capacity installed nationally in Q3 2025.

- Ohio: As the heart of the re-industrialization effort, Ohio is consuming vast quantities of wire mesh for new semiconductor and EV battery factories in the US cold drawn wire market. The state’s strong automotive base also supports high demand for CHQ wire.

- Florida: Hurricane resilience drives consistent consumption here. Following recent storms, US$ 600 million was allocated in October 2024 for grid resilience in impacted areas. Housing starts also remain strong, necessitating mesh for concrete foundations.

- Georgia: Rapid industrialization, particularly in the EV supply chain, has turned Georgia into a major buyer. The state is a key beneficiary of the US$ 234 billion manufacturing boom, with massive factory footprints requiring extensive reinforcement.

Emerging Trends: Grid Modernization and Renewable Energy

Future growth avenues for the US cold drawn wire market are increasingly tied to energy transition initiatives. The Grid Resilience and Innovation Partnerships (GRIP) program is currently deploying US$ 10.5 billion in grants for the 2024/2025 cycle. In August 2024, the Department of Energy awarded US$ 2.2 billion to eight major resilience projects, followed by another US$ 2 billion for 38 projects in October. These investments have sparked a total public-private commitment valued at US$ 4.2 billion. Utility operators are aggressively sourcing ACSR core wires and guy wires to harden networks against extreme weather.

Renewable energy deployment offers a parallel opportunity for the players in the cold drawn wire market. Forecasts indicate 33.3 GW of utility-scale solar capacity will be installed in 2025, with 21.3 GW scheduled for the second half of the year. Solar projects require miles of fencing and racking wire. The sector set a record with 30 GW installed in 2024, and solar plus storage accounted for 85% of all new power added to the US grid in the first nine months of 2025. Domestic manufacturing is responding, with 4.7 GW of new solar module capacity coming online in 2025, further localizing the supply chain.

Import Dynamics and Raw Material Volatility

International trade and input costs continue to shape the competitive landscape of the US cold drawn wire market. Domestic producers are currently navigating a volatile raw material environment. Chicago shredded scrap prices climbed to US$ 388 per gross ton in January 2025, up from US$ 368 in December 2024. Ferrous scrap grades saw an absolute increase of US$ 20 per ton. Nucor listed its HRC base price at US$ 750 per ton in early 2025. These rising input costs put pressure on domestic margins, potentially making imports more attractive despite tariffs.

Logistics add another layer of complexity to the import/export equation. Moving heavy wire products remains expensive in the US cold drawn wire market, with national flatbed spot rates hitting US$ 2.39 per mile in January 2025. Contract rates were even higher at US$ 3.06 per mile. With truck volumes forecast to grow 1.6% in 2025, transport costs are projected to rise, with flatbed spot rates expected to reach US$ 2.61 per mile by June 2025. Consequently, regional sourcing is becoming a strategic priority. Buyers are increasingly looking to near-shore suppliers or domestic mills like Nucor—which deployed US$ 3.2 billion in CapEx in 2024—to mitigate freight risks and ensure timely delivery for critical infrastructure projects.

Segmental Analysis

Cost Effective Carbon Grades Anchor Massive Automotive and Infrastructure Production Volumes

Carbon steel dominates the US cold drawn wires market with a 51.42% share, primarily because it remains the economic backbone for high-volume industries. Manufacturers in the US cold drawn wire market heavily favor these grades as they offer the necessary strength for automotive frames without the exorbitant costs associated with exotic alloys. Domestic production of light vehicles is on track to hit 10.45 million units in 2025, generating a consistent need for carbon steel seat frames and fasteners. To support this volume, Liberty Wire Johnstown recently injected USD 250 million into their facilities, specifically targeting increased capacity for standard carbon grades. Beyond the factory floor, the sector is being propelled by the Infrastructure Investment and Jobs Act, which has allocated USD 110 billion strictly for roads and bridges. These massive civil engineering projects create a direct pipeline for carbon steel demand, as engineers specify it for concrete reinforcement and suspension cables.

The momentum continues into the broader construction and rail sectors, where carbon steel proves indispensable. Industry data suggests that new construction projects now account for 40% of annual steel consumption, a figure heavily weighted toward carbon wire mesh and structural reinforcements. The US cold drawn wire market is further buoyed by federal initiatives earmarking USD 66 billion for passenger and freight rail expansion, which relies on carbon steel for track fasteners and signaling hardware. On the housing front, builders completed over 500,000 multifamily units in the last cycle, all of which necessitate extensive wiring for structural integrity.

- Tesla reportedly secured supply chains for 18,000 metric tons per year of specialized carbon steel for truck production.

- Estimates indicate that every USD 1 billion in infrastructure spending necessitates 50,000 net tons of steel products.

- Recent trade policies imposed a 50% tariff on specific non-carbon imported wire products, steering buyers back to domestic carbon steel.

Automotive Suspension and Grid Modernization Projects Rely On Medium Diameter Versatility

The medium size range (2.0–6.0 mm) secures a solid 38.97% share by serving as the "Goldilocks" gauge for both heavy industry and residential needs. In the US cold drawn wire market, this specific thickness is vital for automotive seat structures, with Michigan plants concentrating production on 5.5mm diameter specifications. Concurrently, the energy sector is driving demand, as Pittsburgh steelmakers have ramped up 6mm wire production designed specifically for AP6 offshore wind foundations. The sheer scale of the USD 39 billion allocated for public transit infrastructure also supports this segment, as security fencing around these new hubs predominantly utilizes medium-gauge wire. Moreover, the 2025 Architecture 2030 mandate requiring a 50-year lifespan for building components pushes engineers toward these thicker, more durable wires over thinner alternatives.

Residential economics further cement the status of the medium diameter segment. With 30-year fixed mortgage rates dipping below 6.0%, a resurgence in home renovation projects has sparked demand for nails and hangers that fall strictly in the 2mm to 6mm range. When rebar prices surged to USD 1,240 per ton, many builders substituted heavy bars with medium-diameter welded wire reinforcement where building codes allowed. The US cold drawn wire market is also reacting to the electric vehicle boom; the USD 7.5 billion federal investment in charging infrastructure relies heavily on medium-gauge wire for internal protective cabling and station components.

- Builders completed approximately 475,000 multifamily units in 2022, creating a sustained baseline for 2mm-6mm wire mesh.

- Imports of construction steel faced a 26% price soar, encouraging domestic sourcing of medium-diameter stock.

- Housing Market Index scores hovering around 40 indicate a focus on essential repair, which utilizes standard medium-gauge hardware.

Cold Heading Applications and Construction Fasteners Sustain High Medium Tensile Demand

Medium tensile grade wire captures 34.33% of the market, functioning as the essential workhorse for applications requiring a balance of strength and flexibility. The US cold drawn wire market relies on these grades (typically 1005–1045) because they can be cold-headed into complex fastener shapes without cracking. This segment generated revenue exceeding USD 9.7 billion within the carbon wire category alone, highlighting its ubiquity. Demand is further solidified by the USD 550 billion in new spending authorized under the bipartisan infrastructure deal, which calls for massive quantities of general-purpose bolts and rivets. Even automakers have established a 200 MPa minimum tensile threshold for specific battery fasteners, a requirement that medium tensile wire meets perfectly without the brittleness found in higher grades.

Beyond heavy industry, the versatility of medium tensile wire keeps it in high demand across the agricultural and utility sectors in the US cold drawn wire market. The forecast for the US industrial fasteners market projects it to reach USD 21.1 billion by 2030, a growth trajectory heavily dependent on medium tensile feedstock. Domestic fabricators have increasingly turned to these local grades after recent tariffs of 25% made imported steel less attractive. Furthermore, manufacturers producing for the USD 48.4 billion drinking water infrastructure allocation prioritize medium tensile stainless and carbon wires, valuing their ability to withstand installation stress while maintaining form.

- The automotive steel market is projected to reach USD 20.5 billion by 2030, with medium tensile grades forming the bulk of non-structural components.

- Spending on residential construction renovation supports steady consumption of medium tensile nails and screws.

Customize This Report + Validate with an Expert

Access only the sections you need—region-specific, company-level, or by use-case.

Includes a free consultation with a domain expert to help guide your decision.

Continuous Manufacturing Shifts Production Lines Toward Efficient Coiled Wire Utilization

Coiled wire (spools) commands a substantial 58.70% share, a dominance explained by the relentless industrial push for automation and speed. Factories operating within the US cold drawn wire market are increasingly transitioning to continuous-feed machinery to minimize downtime. The US industrial fasteners market, which feeds directly off these coils, generated revenue exceeding USD 17.7 billion in 2024, proving that high-speed heading machines are the industry standard. Facilities that have integrated smart manufacturing sensors with coiled feed lines reported reducing downtime by 34%, a critical efficiency gain that cut-length wire simply cannot match. Furthermore, the burgeoning "EV Highway" corridor now represents 38% of regional wire demand, where battery pack assembly lines rely on continuous wire spools for uninterrupted welding and connecting.

Economic pressures also dictate the preference for coils, as manufacturers look to optimize every cent of material cost. With the average age of vehicles on US roads reaching 12.6 years, the aftermarket for replacement springs and fasteners—produced from coiled stock—has exploded. Homebuilders, facing a USD 14,000 increase in material costs per home, are prioritizing coiled wire for nails and mesh because the continuous process significantly lowers scrap rates. Consequently, the US cold drawn wire market sees coil adoption as a financial necessity rather than just a technical preference.

- USD 18.7 billion worth of annual construction steel imports arrive primarily in coiled formats to maximize shipping density.

- Smart manufacturing adoption is expected to reach 25% of production capacity by 2030, necessitating spool-fed automated lines.

- Wire rod prices, the primary feedstock for coils, dropped 2.5% in early 2025, improving profit margins for coil converters.

To Understand More About this Research: Request A Free Sample

Competitive Landscape: Strategic Consolidation and Vertical Integration Define Intense Competitive Wire Market Rivalry

The US cold drawn wire market operates under a rigid, top-heavy structure where the three dominant powerhouses command nearly 29% of the total market share, creating formidable barriers for regional competitors. ArcelorMittal stands as the undisputed market leader, wielding a commanding 14.03% share by leveraging its immense global supply chain to secure high-volume automotive contracts that smaller mills simply cannot fulfill. This concentration of power signifies a maturing industry where efficiency is strictly dictated by volume and feedstock control. The intensity of competition has shifted from simple price wars to a battle for supply chain supremacy; with raw material costs fluctuating in early 2025, these giants utilize their massive purchasing leverage to squeeze margins, forcing independent converters to either specialize in niche alloys or face inevitable acquisition.

Defining the landscape alongside ArcelorMittal are Nucor Corporation and Bekaert, who collectively help shape the cold drawn wire market's strategic trajectory. Nucor continues to aggressively capitalize on the USD 110 billion federal infrastructure injection, utilizing its vertically integrated EAF mills to guarantee feedstock availability for construction-grade wire despite market shortages. Meanwhile, Bekaert secures its stronghold through technological superiority in advanced coatings and high-tensile applications, dominating critical energy and tire reinforcement sectors that demand precision over pure volume. As these three entities drive innovation and capacity expansion, they effectively set the pricing benchmarks and quality standards that the rest of the US cold drawn wire market must follow to survive the current cycle.

Recent Developments in the US Cold Drawn Wire Market

- Insteel Acquisitions: Insteel acquired Engineered Wire Products assets for $67-70 million in October 2024 and O'Brien Wire Products assets for $5.1 million on November 26, 2024, expanding welded wire reinforcement for construction. These moves enhance Midwest and Texas market positions.

- Liberty Peoria Idling: Liberty Steel USA idled its Peoria, Illinois wire rod plant starting December 6, 2024, furloughing over 500 employees amid low-priced imports; restart planned for early 2025 (actual restart March 2025).

- Tree Island Steel Tariffs: Tree Island Steel's Q2 2025 revenue fell to $42.3 million (net of freight), citing U.S. tariffs reducing sales volumes and forcing supply chain shifts.

- Liberty HQ Relocation Plans: Liberty Steel proposed relocating U.S. headquarters from Texas to Peoria area in July 2025, seeking $25 million Illinois grant tied to 700 jobs and $40 million investment.

- Leggett & Platt Restructuring” Leggett & Platt's 2024 restructuring in Bedding Products targets $40-50 million annualized EBIT benefits by late 2025 via wire mill optimization and footprint adjustments for demand alignment.

Top Companies in the U.S. Cold Drawn Wire Market

- Nucor Corporation

- Bekaert

- ArcelorMittal

- Brookfield Wire, LLC

- WCJ Pilgrim Wire

- Ulbrich Stainless Steels & Special Metals, Inc.

- Capital Steel & Wire, Inc.

- California Fine Wire Co.

- Alabama Wire, Inc.

- BCG Wiremesh

- Stalder Spring Works

- Other Prominent Players

Market Segmentation Overview

By Material/Alloy

- Carbon Steel (Low, Medium, High C)

- Alloy Steel

- Stainless Steel

- Non-Ferrous (Copper, Brass, Aluminum, Bronze)

- Others

By Product Form

- Coiled Wire (Spools)

- Straightened & Cut Wire (Rod/Blank)

- Drawn Bars/Wire Rod (Intermediate)

By Diameter/Size Range

- Micro / fine (<0.5 mm)

- Small (0.5-2.0 mm)

- Medium (2.0-6.0 mm)

- Large (>6.0 mm) Industrial

By Mechanical / Performance Grade

- Low Tensile / Annealed

- Medium Tensile

- High Tensile / Cold-Worked / Prestressed

- Specialty (Spring, Bearing, Oil-Tempered)

By Surface Finish / Treatment

- Bright / Polished

- Coated (Zn / Zn-Ni / Phosphate / Polymer)

- Lubricated (Drawing Lubricant)

- Pickled/Annealed

By End-Use / Application

- Automotive

- Construction & Building

- Industrial Machinery

- Oil & Gas / Energy

- Electrical / Electronics

- Fasteners & Hardware

- Medical

- Consumer Goods

- Aerospace

- Others

By Distribution Channel

- Direct Sales

- Distributors / Service Centers

- Metal Service Centers

- Online / E-Commerce (Industrial Marketplaces)

By Region

- Northeast

- Midwest

- South

- West

LOOKING FOR COMPREHENSIVE MARKET KNOWLEDGE? ENGAGE OUR EXPERT SPECIALISTS.

SPEAK TO AN ANALYST

.svg)

Features | Type of License | ||||

Data Book | Single User |   Multi User | Corporate | ||

| e-Access | ✓ | ✓ | ✓ | ✓ | |

User Sharing | 1 User Only | 1 User Only | Up to 7 Users | Unlimited User Access | |

⨉ | ⨉ | ⨉ | ✓ | ||

Free Customization | No Free Customization | Up To 30 hrs work | Up To 60 hrs work | Up To 80 hrs work | |

Deliverable |

| ⨉ | ✓ | ✓ | ✓ |

| ✓ | ⨉ | ✓ | ✓ | |

| ⨉ | ⨉ | ⨉ | ✓ | |

Analyst Support | 2-Months Analyst Support | 4-Months Analyst Support | 7-Months Analyst Support | One Year Analyst Support | |

Free Report update in next update cycle | ⨉ | ⨉ | ⨉ | ✓ | |

Free Industry Update (Within 180 days) | ⨉ | ⨉ | ⨉ | ✓ | |

Benefit | Up to 10% off on Post Purchase | Up to 20% off on Post Purchase | Up to 30% off on Post Purchase | Up to 40% off on Post Purchase | |